OUR BUSINESS

Business Lines

-

REAL ESTATE INVESTMENT

BROKERAGE AND REAL ESTATE CONSULTING

(INCLUDING TRUST BENEFICIARY INTEREST) -

REAL ESTATE RELATED INTERPRETER

-

REAL ESTATE RELATED M&A

ADVISORY SERVICE

REAL ESTATE INVESTMENTBROKERAGE

REAL ESTATE CONSULTING

Based on the principle of trust, win-win and long-term cooperation, as a one- stop partner of investors, our professional team provides investment advice in line with the market and property to ensure the “profitability” and “stability” for investors.

Our company is not a registered Financial Instruments Business Operator (Investment Advisory and Agency business, Investment Management business).

We can introduce such registered Financial Instruments Business Operator if needed.

Real estate trust beneficiary rights and investment structure

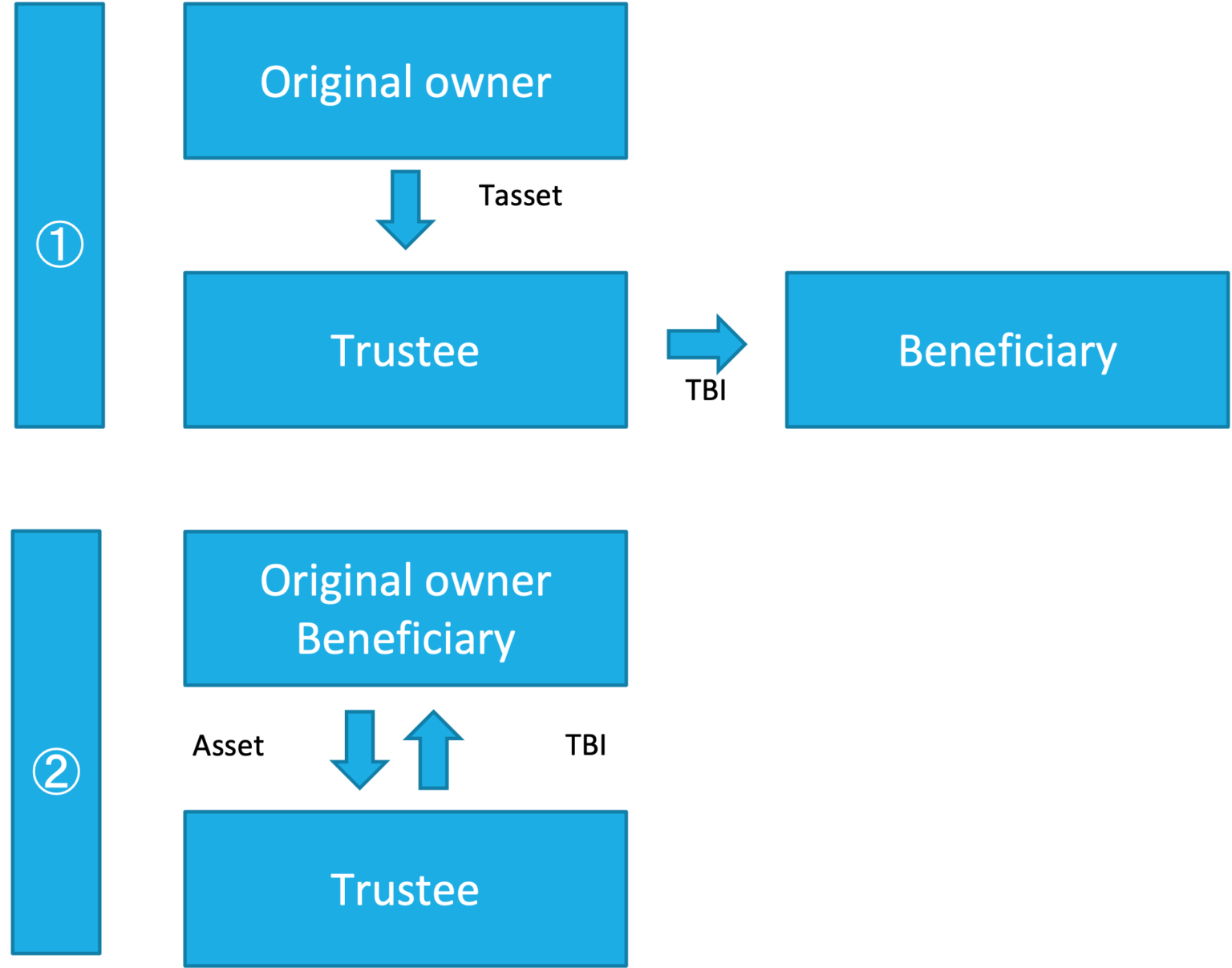

What is Real Estate Trust Beneficial Interest (TBI)?

- The legal basis for the beneficial rights of real estate trusts is the Trust Law promulgated in 1922.

Real estate Trust Beneficial Interest is also known as TBI. - In the trust structure, the relationship between the original owner, the trustee and the beneficiary is as follows.

- The trustee is the legal owner of the trust asset.

In Japan, only trust banks or trust companies licensed by the Finance Department can become trustees. - Beneficiaries are entitled to the economic benefits of trust assets.

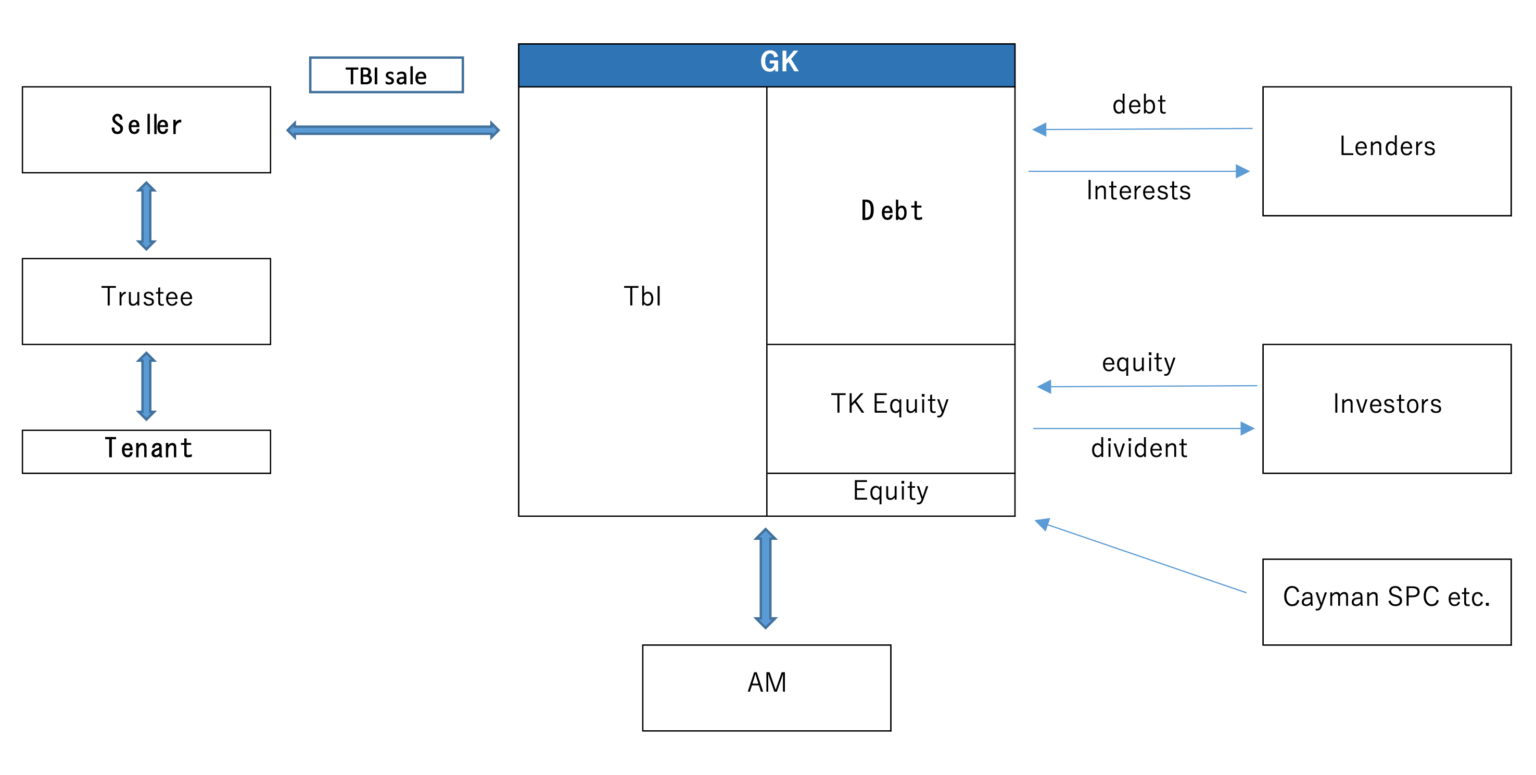

TK-GK

Avoidance of double taxation :

If the TK arrangement is qualified,

the GK is permitted to deduct distributions to the investor from its taxable profits in addition to deducting debt payments.

- TK is the equity investor and GK is the operator. A Tokumei Kumiai (TK) is a contractual arrangement formed under a TK agreement between the GK as operator and the TK investor, as a way of creating equity-like investments. The TK investor contributes funds to the GK (TK Operator), in exchange for a share in the profit/loss of the TK business. The TK should be a Silent Partnership.

- A TK arrangement qualifies for favorable tax treatment if the TK investor is a passive investor with minimal control over the management of the GK and the contributed funds under the arrangement.

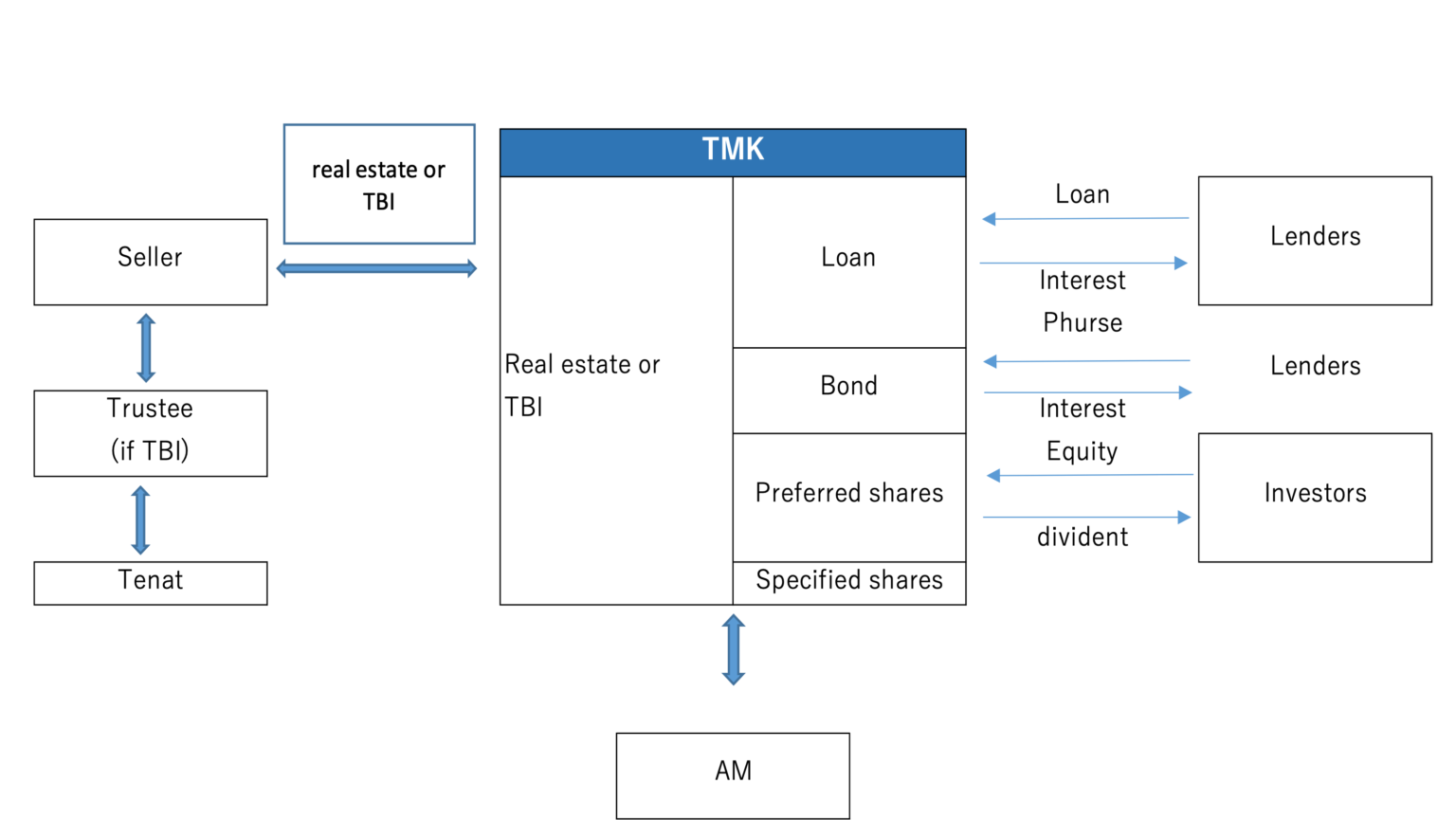

TMK

Avoidance of double taxation :

The TMK distributes more than 90% of the dividends available to investors,

it can deduct such distributions from its taxable profits as an expense.

- TMK can raise funds to purchase real estate by issuing equity to investors. The equity is called Preferred Investment Securities.

- As part of the funding, TMK typically also borrows from banks or other financial institutions.

In order to meet one of the conditions to avoid double taxation, TMK usually needs to issue bonds called Specified Bonds. - Like the TK-GK structure, the investment management is outsourced to asset management companies.